Finding a good health insurance policy can be a daunting task. It can take hours of research, or even weeks. Because of this research, many people wait and do not take insurance. We will simplify this effort for you and compare the top five plans available in India, that is, whatever is in the top five at this point. We will also look at the data.

When we say data, we will look at the claim settlement ratio, whether there are any complaints, what features are in that policy, whether there are good features, and how their pricing is, and we will look at everything in detail. Watch this video till the end. If you look at all the plans, you will understand that they have such features. You will also know what questions to ask. At the end of this post, you will be able to confidently decide which plan is right for you and which plan is right for your situation.

Top 5 health insurance plans india

First and foremost, I am not a financial advisor or an insurance advisor. This is data compiled from online resources and my research. This is just guidance, and there is no recommendation for any of the products that may come up here. You should decide what suits you best for your situation. A zero in this rating means bad, and a zero means great. Now, let’s add these two ratings and compare their prices and give a final rating.

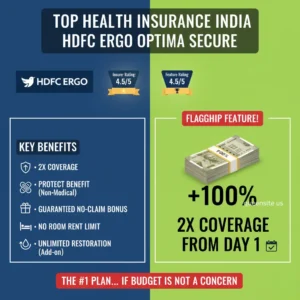

1. HDFC Ergo Optima Secure

Now let’s start with the top five plans of Direct. In the first place is HDFC ERGO Optima Secure. HDFC ERGO is the company name; Optima Secure is the name of the plan. Here the rating of the insurance company is 4.5. This is the top-rated. Here we can see how their claim settlement ratio, complaints to volume, and solvency ratio are in this matrix.

Next, the feature rating of this policy is also 4.5. Earlier, the Optima Restore policy from HDFC was the best seller. Because its features were very good. Now Optima Secure has become the best seller by giving better features than that. The most attractive feature of this policy is that it gives us extra double the coverage from the very first day of purchase. That is, if you have taken a plan with coverage of ₹10 lakh, from the first day they will add another ₹10 lakh extra as ‘secure benefit’ to us. That means we have a total coverage of ₹20 lakh.

Next, in many policies, only medical costs and doctor costs are covered. They do not cover non-medical items. When they say non-medical items, they will bill you for things like gloves, bandages, syringes and so on separately. But in this plan, they will cover all this without any extra cost by calling it ‘Protect Benefit’. Every year after that, you will get 50% extra coverage bonus.

That is, if you take a policy of ₹10 lakh, after the completion of one year, the extra ₹5 lakh will be added. But the maximum will be added only up to 100%. That is, the bonus will be added up to a maximum of ₹10 lakh. In many policies, they say that they will give you a bonus for the next year only if you do not make a full claim in a year. Here, whether you make a claim or not, this bonus will be added to you.

There is no limit on room rent in this plan. No matter which room you stay in, you will be fully covered. Similarly, there is no co-pay class, and there is no limit on disease-wise sub-limit. If we take a plan like Uswala, it is very important to take it without such a limit. They will provide coverage for alternative medicines like Ayurveda and Unani. Along with this, there is a one-time restoration cover per year.

That is, if we get a lot of medical bills in the middle and our coverage is empty, they will also do a complete restoration. If you have paid some extra money and added an add-on, you can also change this to unlimited restoration. That is, they will refill it again and again even if it is empty.

2. Care Supreme

Coming back to the list, Care Supreme is in second place. The feature rating is very good in this plan too. But even when you look at the insurer’s rating, HDFC ERGO is very low. Their advantage is affordability. That is, the cost of the policy is very low. So, overall, they are in second place according to the final rating. We can also see their claim settlement ratio, complaints, and other metrics here.

Care is the name of the insurance company, and its best-selling product is Supreme. The top feature of this plan is unlimited restoration cover. That is, they will automatically refill it every time the tank is empty. Similarly, there is no sub-limit. There is no room rent limit, co-pay class, disease limit, etc. In this plan, whether you make a claim or not in a year, you will automatically get a bonus when you go to the next year.

You will get a bonus of up to 50%. Here too, you can take it up to a maximum of 100%. If you pay a little extra money and add an add-on, you will get an additional 100% bonus. This time, you can extend it up to 500%. That is, if you take a policy with a coverage of ₹10 lakhs and add this add-on, and if you renew it continuously for five years, you will have a coverage of up to ₹60 lakhs through bonuses.

A big advantage of this policy is its cost. When compared to Optima Secure, you will get a discount of 30 to 50%. For example, if a 28-year-old person lives in a city like Bangalore, Optima Secure will cost around ₹13,800 per year. If we compare it with Care Supreme, it will cost around ₹9,000. The negative thing about them is that the claim settlement is not that smooth. Similarly, their complaints are also high when compared to HDFC ERGO.

3. Aditya Birla Activ One Max

Next up is Activ One Max from Aditya Birla. Although the features are not super duper, the insurer’s quality and affordability are good. There are no limits in this policy either. There are no restrictions like room rent limits, co-pay classes, or disease-wise sub-limits. The plus point of this is that you get unlimited restoration benefits. That is, even if our coverage ends, every bottle will be refilled, unlimited.

You get one free health checkup per year. Similarly, when you renew the policy, you get a bonus of up to 100%. Whether you make a claim or not, this bonus will be there. They will say that for that and set a specific limit. You can take coverage up to a maximum of ₹3 crore. Alternative medicines like Ayurveda and homeopathy also have coverage.

If I have to say a feature that you need to be a little careful about, it is the waiting period for pre-existing illness. Usually, if we already have any complaints related to BP, diabetes, heart, etc., if we want to make a claim related to that, there will be a waiting period for that. Most policies have a period of two to three years. Here, the waiting period for pre-existing complaints is three years.

4. Niva Bupa ReAssure 2.0

Next up is the ReAssure 2.0 Platinum or Platinum Plus variant from Niva Bupa. Both these variants offer sufficient coverage at a lower cost. You can buy this policy at a lower price with top-notch features. However, the insurer’s quality rating is low. If I were to name a feature that can be highlighted, they offer something called ‘Age Lock Benefit.’ That is, all these health insurance policies usually increase in price as we age.

The premium will increase even after we buy it. Whatever premium you paid in the beginning, you can continue with the same premium. This is applicable as long as you do not claim. That is, no matter how many years you do not claim, you can continue with the premium you have taken. But after you claim, this premium also starts to increase as per your age.

Here too, there is no co-payment class, no room rent limit, and no sub-limit according to disease. You get unlimited restoration benefits and free health checkups. They also provide coverage for alternative medicine like Ayurveda and homeopathy treatments. We can also see their claim settlement ratio and complaints matrix here. They also have a three-year waiting period for pre-existing diseases.

5. ICICI Elevate

Next up is the Elevate plan from ICICI Lombard. Although their feature rating and affordability are good, their insurer rating is low. One of the main reasons for this is that their claim settlement ratio is not that high. A great advantage of this plan is that even though their base variant does not have many features, the add-ons add on, this plan becomes exceptional.

For example, if you add the ‘Jump Start’ add-on, there will be a specific waiting period for pre-existing diseases. In this plan, it is three years. Three years is a bit too long. However, if you had added this add-on for the diseases you can see here, the three-year waiting period would have been reduced by 30 days. This is a very good feature. There are many more add-ons like this.

If I have to say the good features of this plan, then there is no co-pay class in this one. That is, they will pay the entire bill themselves. There is no need for us to split the bill. Similarly, there is no disease-wise sub-limit. They will cover all possible diseases. They also provide unlimited restoration. That is, even if we make a claim in the same year and our coverage runs out, it will be refilled again. This policy also covers alternative medicines.

If I have to say the negative of this, there is no unlimited room rent limit. That is, if there is a situation where we have to be admitted to the hospital, they will cover only up to the cost of a single private room. If you want to cover pre-existing diseases, you have to wait for at least three years. There is no free health checkup in this policy. If you want to get a free health checkup, you will have to add a separate add-on for it.

We have reviewed all the five plans we have seen so far. If you want to know which one to choose from this list, or if there is a better plan for your situation, schedule a call with the Ditto team and ask all your questions. This call is 100% free of cost. No spamming will happen. You can ask your questions to IRDAI-certified experts. More than 10,000 customers have given it a 4.9 rating. Ditto is the highest-rated insurance advisor in India. Thank you, guys.